Mastering the Sales Comparison Approach

At its core, the sales comparison approach is all about figuring out a property's value by looking at what similar, nearby homes have recently sold for.

It’s really just common sense. If you were selling a used car, you wouldn't just pull a price out of thin air. You'd check what other cars of the same make, model, year, and condition have recently sold for. This is the exact same logic applied to real estate, and it’s why it's the most trusted way to pin down a home's current market value.

The Bedrock of Property Valuation

The entire approach is built on a simple economic idea called the principle of substitution.

This principle says that a savvy buyer won't pay more for one property when they could buy a very similar one down the street for less. It’s a powerful idea because it anchors the valuation process in what real people are actually doing—what they're willing to pay in the current market.

This method isn’t just an abstract theory; it's the engine that powers every Comparative Market Analysis (CMA). It’s what separates a professional valuation from a simple guess.

The Key Players: Subject and Comps

Breaking it down, the process really revolves around two key elements:

- The Subject Property: This is the home we're trying to put a price on. We need to know everything about it—square footage, number of bedrooms and baths, its overall condition, any recent upgrades, and of course, its location.

- The Comparables (or "Comps"): These are the recently sold properties that are as similar to the subject property as we can find. The closer the match, the more accurate our final number will be.

By carefully analyzing the sale prices of these comps, we can make an informed, data-backed estimate of what the subject property is worth.

This isn’t a new concept. For decades, the sales comparison approach has been the gold standard in residential real estate. The standard operating procedure is to find at least three solid, recently sold comps to build a reliable valuation.

It’s the most direct reflection of the market because it’s based on real, closed transactions. To see how this fits into the broader picture, it's helpful to understand the other Top Real Estate Property Valuation Methods that professionals use. Ultimately, this approach gives us a practical, real-world framework for understanding a home's true standing in today's market.

How to Select the Right Comparable Properties

Finding the right "comps" isn't just a box you tick; it’s the absolute bedrock of a credible market analysis. Your entire valuation hinges on the quality of the properties you choose to support it. Think of it like a lawyer building a case—your comps are the star witnesses, and they need to be rock-solid.

This isn't about just pulling a few recent sales. It's about thinking critically and understanding why a property is—or isn't—a good comparison. The real goal here is to vet every potential comp with the sharp eye of an appraiser, making sure your final valuation is built on a foundation that can't be questioned.

The Three Pillars of a Strong Comp

To make sure you're truly comparing apples to apples, every potential comp needs to pass three key tests: proximity, timing, and similarity. These pillars are the cornerstones of a reliable analysis. If a property fails on even one of them, it’s probably not the right fit.

Let’s dig into what makes each one so crucial.

Proximity: We all know the mantra: location, location, location. A genuinely comparable property has to be close by—ideally in the same neighborhood or subdivision, or at the very least, sharing the same school district. A house that's just a quarter-mile away but on the other side of a busy highway might as well be in a different world from a market perspective.

Timing: Markets are always in motion. A sale price from last year is a snapshot of a market that no longer exists. The best comps are always the most recent, usually sold within the last three to six months. In a hot market where prices are climbing fast, you might need to tighten that window to just 90 days to get a truly accurate picture.

Similarity: This is all about the house itself. You’re looking for homes that mirror the subject property in style, age, square footage, bed and bath count, lot size, and overall condition. You simply can't compare a beautifully restored 1920s craftsman to a brand-new build next door and expect an accurate outcome, even if they share a property line.

At its heart, the sales comparison approach relies on the principle of substitution. This concept says that a reasonable buyer won't pay more for a property than what it would cost to buy a similar substitute. Your job is to find comps that a real buyer would see as a legitimate alternative.

Vetting Comps Like a Pro

Once you've pulled a list of potential comps that seem to fit the bill, the real work begins. It’s time to dig deeper, verify the data, and understand the story behind each sale. A quick skim of an MLS sheet just won’t cut it.

For instance, was the sale a standard, open-market transaction? Or was it sold between family members for a friendly discount? Maybe the seller was in a tough spot and had to sell fast for a job relocation. These circumstances can throw the sale price way off and make a property a poor comparable.

Your mission is to find sales that reflect genuine market conditions, free from any special circumstances. This is the kind of diligence that separates a quick guess from a professional, trustworthy valuation.

Making Adjustments to Your Comparables

This is where the real work begins—the part where a valuation goes from being a simple comparison to a refined analysis. Once you’ve picked your best comps, you have to account for all the little (and big) differences between them and your subject property. After all, no two homes are identical. Adjustments are how we level the playing field.

Think of it like a handicapping system in sports. You give or take points to make the matchup fair. In real estate, we assign a dollar value to the differences, figuring out what each comp would have sold for if it were a mirror image of the property we're valuing. This critical step turns a list of sale prices into a strong, justifiable estimate of value.

These aren't just wild guesses. Each adjustment is a calculated estimate rooted in what the local market is actually paying for specific features.

The Logic of Adding and Subtracting Value

The golden rule of adjustments is simple: Always adjust the comparable property, never the subject property. The entire goal is to make the comp look more like your property on paper.

Here’s how it works:

- If the comp is superior to your property (it has a finished basement and yours doesn’t), you subtract the value of that feature from the comp’s sale price.

- If the comp is inferior to your property (yours has a brand-new kitchen and the comp’s is dated), you add the value of that feature to the comp’s sale price.

This process is a mix of art and science. A professional appraiser, for instance, will adjust a comp’s price downward if it has an extra bedroom the subject property lacks. On the flip side, they’ll adjust the value upward if the subject property has a desirable feature, like a three-car garage, that the comp is missing. It’s all about creating an apples-to-apples comparison.

Tangible Versus Intangible Adjustments

Adjustments typically fall into two buckets: the stuff you can easily put a price on and the things that are a bit more subjective.

Tangible Adjustments cover the physical features with a fairly clear market value. These are the black-and-white line items.

- Gross Living Area (GLA): The home's total square footage.

- Room Counts: Differences in the number of bedrooms or bathrooms.

- Garage: A two-car garage versus a one-car, or no garage at all.

- Major Upgrades: A fully renovated kitchen, a new roof, or an updated HVAC system.

- Amenities: A swimming pool, a fireplace, or a finished basement.

Of all these, property size is often the most significant factor. That's why accurately calculating square footage is so crucial to getting the valuation right.

Intangible Adjustments are for features that definitely impact value but don’t have a standard price tag. Their worth is all about buyer perception.

- Location: A desirable corner lot versus a mid-block property.

- View: Backing onto a quiet park versus facing a noisy intersection.

- Condition: The overall upkeep and curb appeal. A pristine home will always command more than a fixer-upper.

- Financing Terms: Unconventional financing (like seller concessions) that might have inflated a sale price.

The most important thing to remember is that every adjustment needs to be backed by market evidence. An agent can't just decide a great view is worth $15,000. They have to find data from the local market—often through a technique called paired sales analysis—that supports that number.

Let's look at a simplified example of how this plays out in an adjustment grid. This is how we organize the data to see the final adjusted prices side-by-side.

Sample Adjustment Grid for a Subject Property

| Feature | Subject Property | Comparable 1 | Adjustment | Comparable 2 | Adjustment |

|---|---|---|---|---|---|

| Sale Price | - | $350,000 | $340,000 | ||

| Lot Size | Standard | Standard | $0 | Larger | -$5,000 |

| Bedrooms | 3 | 3 | $0 | 3 | $0 |

| Bathrooms | 2 | 2.5 | -$4,000 | 2 | $0 |

| Garage | 2-Car | 1-Car | +$6,000 | 2-Car | $0 |

| Condition | Good | Excellent | -$7,000 | Good | $0 |

| Adjusted Price | $345,000 | $335,000 |

By applying these adjustments line by line, you can see how we systematically narrow the gap between the properties. The adjusted prices of $345,000 and $335,000 give us a much tighter and more reliable range to determine the subject property's true market value.

Your Step-by-Step Valuation Workflow

Alright, let's put all the pieces together. The sales comparison approach isn't just some abstract theory; it's a practical workflow. When you get it right, the result is a valuation that’s not only accurate but also easy to defend.

Think of the following five steps as your roadmap. Each one builds on the last, guiding you from a starting point to a solid, evidence-backed conclusion. This is how you bring order and clarity to the often-messy process of property valuation.

Step 1: Define the Subject Property

Before you even think about looking for comps, you need to know the subject property inside and out. This property is your benchmark—the standard against which every other property will be judged. And I mean every detail.

Go way beyond just the number of beds and baths. Get granular.

- Physical Attributes: Nail down the exact square footage, the year it was built, its architectural style, and the overall floor plan.

- Condition and Upgrades: Has the kitchen been recently remodeled? Is the roof on its last legs? You need to document both the highlights and the potential drawbacks.

- Lot Characteristics: What's the lot size? Is it a corner lot or tucked away on a cul-de-sac? Does it have a killer view or waterfront access? These things matter.

Step 2: Research and Select Viable Comps

Now that you have a crystal-clear picture of your subject property, the hunt for comps begins. The gold standard in the industry is to find at least three solid comparables that have sold within the last six months.

Your go-to resources here are the Multiple Listing Service (MLS) and public records. As you sift through listings, be ruthless with your filters. You're looking for properties so similar that a potential buyer for your subject would have seriously considered them. Proximity, sale date, and physical resemblance are everything.

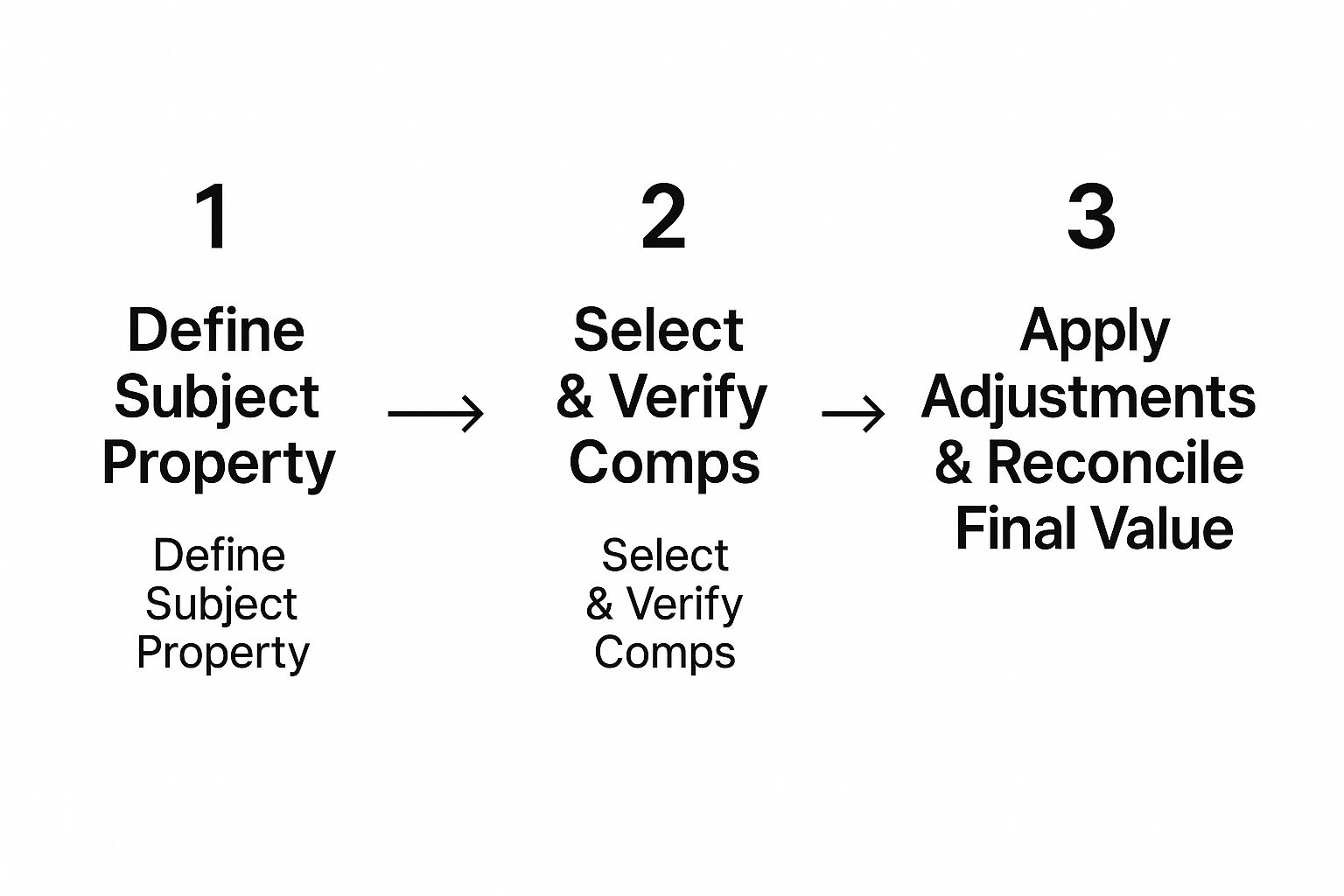

This infographic breaks down the core sequence, from defining the property to arriving at a final value.

As you can see, it's a logical progression. Each step informs the next, building a case for your final valuation.

Step 3: Verify All Comp Data

Here's a step many people get lazy on, but it’s absolutely critical: never take listing data at face value. Always verify the details for each comparable sale you've chosen.

Public records are great for confirming the final sale price and closing date, but sometimes you have to dig a little deeper. You need to be sure it was an "arm's length" transaction—meaning the buyer and seller weren't related and neither was under pressure to make a deal. A sale between family members, for instance, isn't a true reflection of market value and should be tossed out.

Step 4: Apply and Document Adjustments

This is where the real analysis happens. You're going to systematically compare each comp to your subject property, feature by feature, and account for the differences.

Just remember the golden rule: always adjust the comp, never the subject. If your comp has a superior feature (like a brand-new kitchen), you subtract value from its sale price. If it's inferior (maybe it has one less bathroom), you add value.

Crucially, you must document every single adjustment you make and provide market-based evidence for the dollar amount you chose. This documentation is what separates a professional analysis from a guess.

The credibility of your entire valuation rests on the quality of your adjustments. Unsupported or arbitrary adjustments are the number one red flag in a weak market analysis. Your reasoning must be clear, logical, and backed by local market data.

Step 5: Reconcile and Determine Final Value

After making your adjustments, you'll be left with a range of adjusted sale prices from your comps. The final step isn't as simple as just calculating an average. That’s a common mistake.

Instead, you need to perform a reconciliation. This means you give more weight to the comps that are most similar to your subject property—the ones that required the fewest or smallest adjustments. They are the most reliable indicators of value.

This weighted analysis leads you to a single, final estimate of value. It's not just a number pulled out of thin air; it’s the culmination of your research, verification, and careful calculations. It’s a market value you can stand behind because it's grounded in solid evidence.

Navigating Challenging Market Conditions

The sales comparison approach is a fantastic tool, but let's be honest—its accuracy hinges entirely on the data you can find. In a perfect world, you'd have a handful of nearly identical homes that all sold last month, right around the corner. But real estate is rarely that clean and simple.

Markets can throw some serious curveballs your way, forcing you to think on your feet. You might be working in a blistering seller's market, a sluggish buyer's market, or with a unique property miles from anything else. These situations don’t mean the approach is broken; they just require you to be more creative and thorough.

Adapting to Market Dynamics

A one-size-fits-all strategy just won't cut it when the market gets weird. You have to adjust your tactics based on the climate you're in.

Hot Seller's Markets: When prices are climbing fast, a comparable from six months ago might as well be from another decade. You have to shorten your time horizon dramatically, focusing on sales within the last 30-60 days if you can. Making those time adjustments becomes absolutely critical to reflect the rapid appreciation.

Slow Buyer's Markets: In a slow market, homes can linger for months. This means you might have to look back over a longer period. More importantly, you need to dig into the gap between list prices and final sale prices to get a real sense of seller concessions and buyer leverage.

Rural or Unique Properties: What do you do when the closest "comp" is five miles away and sold over a year ago? This is a common headache in rural areas or for one-of-a-kind homes, like a historic landmark or an ultra-modern design. A direct, apples-to-apples comparison is often out of the question.

In challenging markets, your role shifts from a data processor to a market detective. You must dig deeper to understand the story behind each number and justify every decision with clear, logical reasoning.

Solutions for Scarce Comparables

When good comps are playing hard to get, you can't just throw in the towel. The trick is to broaden your search strategically while making careful, well-documented adjustments that keep your analysis credible.

The effectiveness of the sales comparison approach can really swing depending on market conditions. In fast-moving markets or areas with low inventory, finding true comps is tough. You might need to expand your search radius, but when you do, be prepared to make strong location adjustments. If you have to reach further back in time, apply market condition adjustments. You can learn more about these detailed discovery methods to sharpen your skills.

Sometimes, the best comps you find won't be perfect matches. You might have to use a property that's quite different but then apply a larger, well-supported adjustment. The absolute key is to document your reasoning for every single tweak you make.

Ultimately, when you’re in a truly complex situation and the sales comparison approach feels stretched thin, it's smart to lean more heavily on other valuation methods. Bringing in the cost or income approach can help you build a much more complete and defensible picture of a property's true value.

Answering Your Top Property Valuation Questions

Even when you have a solid process, the sales comparison approach always seems to spark a few questions. It's a method that walks a fine line between hard data and professional judgment, so it's only natural to wonder about the specifics.

Let's clear up some of the most common sticking points. Getting these details right will help you build your CMAs with more confidence and accuracy.

How Many Comps Do I Really Need?

You've probably heard the magic number is three comparable properties. While that's a decent starting point, the real answer is: it depends. The goal isn't just to check a box; it's to build a valuation that you can stand behind. For a standard house in a subdivision with plenty of recent sales, three to five great comps will usually do the trick. That’s enough data to spot a clear pricing pattern without overcomplicating things.

But what if you're pricing a one-of-a-kind property or a home in a rural area where sales are few and far between? In those cases, you’ll likely need to expand your search, maybe to five, seven, or even more comps. You're building a case, and when each comparable requires bigger adjustments, you need more evidence to support your conclusion.

At the end of the day, it's always quality over quantity. A valuation based on three nearly identical comps is far stronger than one cobbled together from ten mediocre ones that need massive, speculative adjustments.

What's the Difference Between a CMA and an Appraisal?

It’s easy to see why people mix these two up, but they are fundamentally different reports with different purposes and legal standing.

A Comparative Market Analysis (CMA) is a tool created by a real estate agent for their client. It's designed to help a seller land on the right listing price or to help a buyer make a competitive offer. Think of it as an expert opinion on market value, backed by recent sales data.

An appraisal, however, is a formal, legally-defensible opinion of value prepared by a state-licensed appraiser. Lenders require an appraisal to secure a mortgage because it’s a rigorous, impartial assessment that must follow strict guidelines, like the Uniform Standards of Professional Appraisal Practice (USPAP).

Should I Factor in Active or Pending Sales?

This is a great question because it cuts right to the heart of understanding a live market. Closed sales are the foundation of any CMA. They are historical facts—a price has been paid, and the deal is done. These are the only sales you can use as your primary comparables.

But that doesn't mean active and pending listings aren't useful. In fact, they offer a real-time snapshot of the market.

Active Listings: These tell you who you're up against. Looking at the active competition reveals current pricing strategies and how much inventory is on the market.

Pending Sales: These are a gold mine. A pending sale is the most up-to-the-minute indicator of what a buyer in the current market is willing to pay.

You can't use them as one of your main comps—the final price isn't set in stone, and the deal could still fall apart—but they make for powerful supporting evidence. In a fast-moving market where closed sales are already a month or two old, pointing to a recent pending sale can help justify your pricing and show you have your finger on the pulse of where the market is headed.

Ready to create stunning, data-driven CMAs in seconds? Saleswise uses AI to research comps, analyze market data, and generate professional reports that win listings. Stop spending hours on manual analysis and start closing more deals. Try Saleswise for just $1.

Article created using Outrank