How to Do a Comparative Market Analysis

A solid Comparative Market Analysis starts with two key things: a deep dive into your subject property and a hunt for at least three comparable homes—the "comps"—that have sold recently in the same neighborhood. From there, you'll make dollar-value adjustments for any differences in features, size, or condition. This whole process gives you a reliable market value range, which is your anchor for setting a list price or crafting a smart offer.

The Foundation of an Accurate Property Valuation

Before you ever open a spreadsheet or pull a report, it's important to grasp what a CMA really is. It’s not just an educated guess; it's a careful, evidence-based evaluation of a property's current worth. For sellers, it’s the strategic foundation for pricing a home to sell. For buyers, it’s the gut check needed to submit a confident, well-supported offer.

Think of the CMA as your roadmap. It grounds your entire strategy in hard data, taking the emotion and guesswork out of the equation.

Why a CMA Is Essential

A thoughtfully prepared CMA doesn't just spit out a number—it delivers clarity. It directly answers the single most important question in any real estate deal: What is this property actually worth today?

This analysis is a non-negotiable step for a few key reasons:

- For Sellers: It’s all about hitting that pricing sweet spot. You want to attract motivated buyers without leaving any money on the table. Price it too high, and the property just sits. Too low, and you've lost hard-earned equity.

- For Buyers: A CMA gives your offer credibility. It provides the data you need to negotiate from a position of strength and, most importantly, protects you from overpaying in a heated market.

- For Agents: This is where you demonstrate your expertise. A solid CMA shows clients the "why" behind your pricing recommendations, building the trust and credibility that are the cornerstones of your business.

CMA vs Formal Appraisal

This is a common point of confusion, so let's clear it up: a CMA is not a formal appraisal. They serve completely different purposes and carry different weights. As real estate professionals, we create a CMA to help clients develop a pricing strategy. It's an informed opinion of value based on current market activity.

A formal appraisal, on the other hand, is a legally binding valuation conducted by a state-licensed appraiser. Lenders absolutely require one to approve a mortgage because it protects their investment. The process is much more rigid and involves a detailed, in-person inspection.

To put it simply, a CMA is your strategic guide for making smart decisions. An appraisal is an official valuation required by the bank.

Here’s a quick breakdown of the main differences:

CMA vs Formal Appraisal At a Glance

| Attribute | Comparative Market Analysis (CMA) | Formal Appraisal |

|---|---|---|

| Purpose | To guide sellers and buyers on pricing strategy. | To determine a property's value for a lender's mortgage approval. |

| Created By | Licensed real estate agent or broker. | State-licensed or certified appraiser. |

| Legal Standing | An informed opinion of value; not legally binding. | A legally binding valuation for financial transactions. |

| Cost | Typically provided for free by an agent. | Costs several hundred dollars, usually paid by the buyer. |

| Methodology | Analysis of recent comparable sales, active listings, and market trends. | A more rigorous process following strict industry guidelines (USPAP). |

| Client | The home seller or buyer. | The lender who ordered the appraisal. |

Knowing the difference helps everyone understand their role in the transaction.

A CMA is an opinion of value based on current market trends, created to inform strategy. An appraisal is a certified valuation required for financial transactions. Understanding this distinction is key to navigating the real estate process.

The best CMAs rely on the freshest data possible—I’m talking sales from the last 3 to 6 months. Real estate is dynamic. For instance, the U.S. housing market saw a staggering 14.8% year-over-year jump in median home prices in 2022, but that growth cooled to just 3.2% by 2023. This is a perfect example of why timely data is everything. You can read more about what's shaping the market in the Urban Land Institute's global real estate trends report.

Now, let's get into the nitty-gritty of how to build a powerful and accurate analysis from the ground up.

Getting Your Data Straight: The Foundation of a Credible CMA

Let's be blunt: the entire credibility of your CMA hinges on the quality of your data. If you start with faulty information, your final valuation will be flawed, no matter how good you are at making adjustments. This first step is where you have to be meticulous. There are no shortcuts.

For a real estate professional, the primary source of truth is almost always the Multiple Listing Service (MLS). The MLS gives us access to a goldmine of real-time, accurate data that public-facing websites just can't compete with. It's the difference between making an educated guess and knowing.

Get to Know the Subject Property, Inside and Out

Before you can even think about finding comparable homes, you need to build an exhaustive profile of the property you're analyzing. This is about more than just the basic bed and bath count; you're creating a detailed blueprint that captures every single feature that could influence its value.

Start by pulling the hard facts directly from the MLS and public records to get your baseline:

- The Basics: Nail down the exact square footage (both above and below grade), the lot size, and the year it was built.

- Room Counts: Note the precise number of bedrooms and full/half bathrooms. This is a huge value driver.

- Structural Info: Document the property type (single-family, condo, townhouse), number of stories, and garage capacity.

But let's be honest, the raw numbers only tell half the story. The little details are what often justify big price adjustments down the line.

A great CMA tells the property's unique story. It’s not just a three-bedroom house; it’s a three-bedroom house with a kitchen remodeled last year, a south-facing yard perfect for a garden, and a brand-new HVAC system. These details are your ammunition for a sharp, accurate valuation.

You have to dig deeper to find the property's unique selling points and potential red flags. A personal walkthrough is always best, but if you can't swing it, use listing photos, seller disclosures, and a good conversation with the listing agent to uncover details like:

- Recent Upgrades: Has the kitchen been touched in the last five years? Are the windows new? What about the roof?

- Special Features: Look for anything that makes it stand out. A swimming pool, a finished basement, professional landscaping, or a killer view all add to the story.

- Condition and Deferred Maintenance: Be brutally honest here. An aging roof or an old-school electrical panel are just as important to note as a slick, modern bathroom.

Sourcing and Verifying Your Data

Once you have a crystal-clear picture of the subject property, it's time to play detective. Data can get messy, and it’s surprisingly common to find discrepancies between the MLS, tax records, and what the seller remembers. The mantra here is simple: trust, but verify.

The MLS should be your go-to, but don't stop there. Cross-reference the key details with public records, which you can usually find on your county assessor's website. This simple step helps you catch errors that could throw off your entire analysis.

I've seen it happen. I once analyzed a home listed in the MLS as having 2,200 square feet. But when I pulled the tax records, they showed only 1,800 square feet. The culprit? An unpermitted sunroom addition. While it was a nice space, it couldn't legally be counted in the gross living area. Catching that one detail saved my client from overvaluing the property by tens of thousands of dollars.

When you find a discrepancy, dig in. Sometimes it's a simple typo. Other times, it points to a much bigger issue. This verification process is what separates a quick online guesstimate from a professional, defensible analysis that your clients can count on.

With a fully documented and verified profile of your subject property in hand, you're finally ready to tackle the art of selecting the perfect comps.

Selecting and Analyzing Comparable Properties

Choosing the right "comps" is where the science of data meets the art of market interpretation. Once you have a detailed profile of your subject property nailed down, your next job is to find a handful of recently sold homes that are as similar as possible. This selection process is, without a doubt, the absolute core of a credible market analysis.

Think of it like this: you're trying to find the subject property's closest relatives in the market. The more alike the comps are, the fewer adjustments you'll have to make down the line, which directly translates to a more accurate valuation. Your real goal is to find properties that a potential buyer would have legitimately cross-shopped with your subject property.

What Makes a Comp a Good Comp?

Not all sold homes are created equal. To make sure your analysis is built on a solid foundation, you have to run every potential comp through a pretty strict set of filters. Sticking to these guidelines is how you avoid including outliers that can completely throw off your numbers.

A strong comparable property generally has to check these boxes:

- Proximity: It needs to be in the same neighborhood, and I mean really in the neighborhood—ideally within a one-mile radius. In rural areas, you might have to stretch that, but the key is staying within a market that shares the same schools, amenities, and overall vibe.

- Recency of Sale: This is huge. You want to focus on properties sold within the last 3 to 6 months. A sale from a year ago reflects a totally different market and is practically ancient history in real estate terms.

- Size and Layout: Look for similar square footage, usually within a 10-20% variance. A 1,500 sq ft home is just not a good comp for a 3,000 sq ft one—they're in different leagues. The bed and bath count should also line up as closely as possible.

- Age and Style: A 1920s bungalow and a 2010 modern build attract completely different buyers. Find homes built around the same time with a similar architectural style.

Filtering your MLS data using these specific parameters is the most effective way to start pulling together a shortlist of potential candidates.

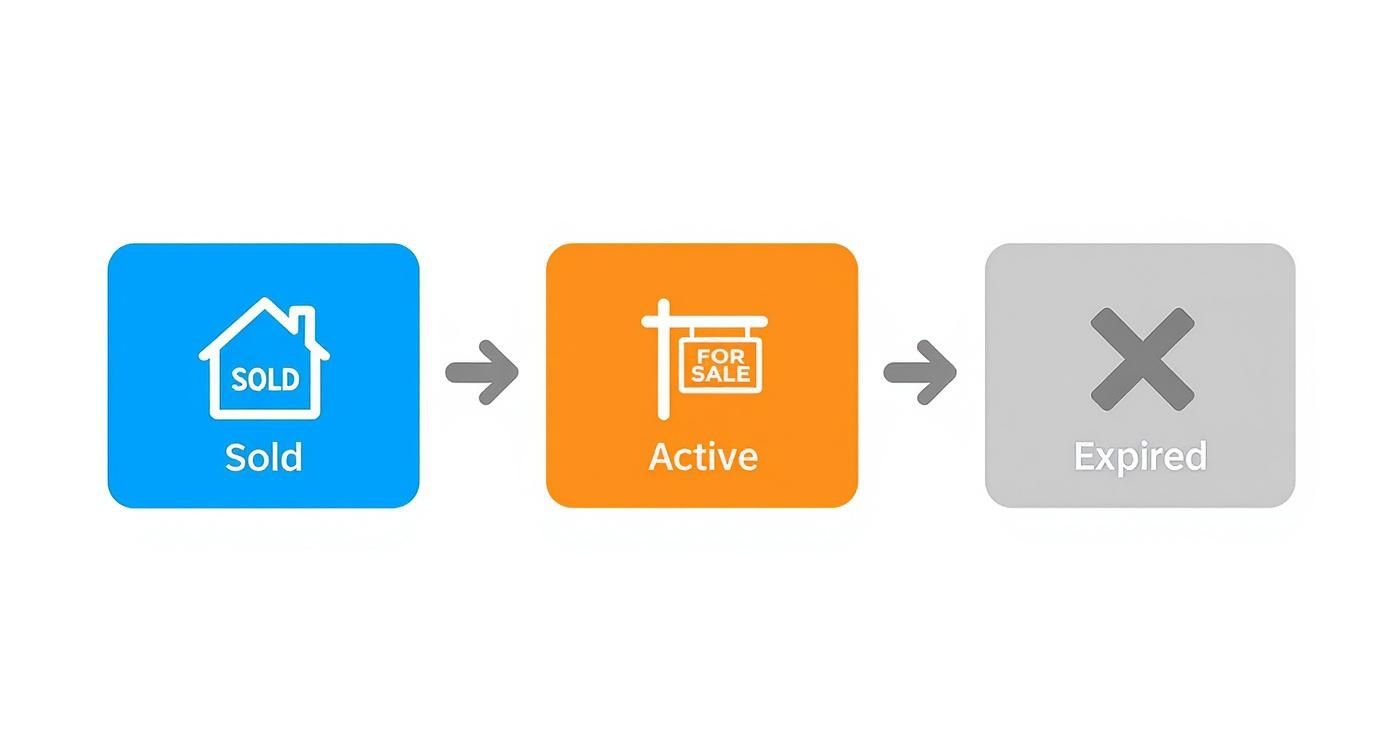

The Three Types of Comps and What They Tell You

A truly comprehensive CMA doesn't just look at what has sold; it also considers what's happening in the market right now. To get the full picture, you really need to look at three distinct categories of properties.

1. Sold Properties These are your bread and butter—the most important data points you have. Sold comps are the hard evidence of what buyers in the real world have actually been willing to pay for homes like yours. They are the factual bedrock of your valuation.

2. Active Listings These properties represent your current competition. Looking at what's actively for sale shows you what other sellers are asking, which is critical for positioning your subject property competitively. If every similar home is clustered around $550,000, coming in at $625,000 is probably a non-starter.

3. Expired or Withdrawn Listings I call these the cautionary tales. Listings that failed to sell almost always tell a story of overpricing. They essentially define the market's price ceiling—the point where buyers collectively said, "Nope, not for that much." Understanding that ceiling is crucial for setting a realistic price right out of the gate.

By looking at sold, active, and expired listings together, you create a 360-degree view of the market. You see what has worked, what isn't working, and exactly where your property fits into the current landscape.

Navigating Unique Properties and Shifting Markets

So, what happens when you just can't find perfect comps? This is a common headache with unique homes or in less-populated areas. When this happens, you have to systematically broaden your search criteria. First, I'd try extending the sale date back to nine or even twelve months. If that well is dry, expand your geographic search to a similar, adjacent neighborhood. You’ll have to make larger adjustments, sure, but that’s far better than working with no data at all.

The way we approach this has certainly evolved. In 2023, for example, Zillow's Zestimate algorithm was used for over 120 million property valuations. These automated models had a median error rate of 2.4% for on-market homes but a much wider 7.5% for off-market ones. For comparison, traditional CMAs by agents typically have a median error rate of 5-10%, which really shows the value of professional nuance—especially when dealing with tricky or unique properties. You can see more on how tech is shaping valuations in this global living report from Hines.

Understanding these different angles is all part of mastering valuation. For a deeper dive into the methodology, check out our guide on the sales comparison approach for more advanced techniques.

Once you have meticulously selected your best three to five sold comps—along with a few active and expired listings for context—you're ready for the next critical step: quantifying the differences and calculating a final value.

Making Adjustments and Calculating Value

Alright, you've cherry-picked your best comps. Now comes the real art and science of the CMA: making adjustments.

It’s the step that separates a quick Zestimate-style guess from a professional valuation. You’ll almost never find a comp that’s a perfect mirror image of your subject property. So, we have to account for the differences, and that's where skillful, defensible adjustments come into play.

Think of it as creating a level playing field. The whole point is to adjust a comparable property's sale price to show what it would have sold for if it had the exact same features as your client's home.

Quantifying the Differences

This isn't about pulling numbers out of thin air. Good adjustments are always backed by market data. You're essentially answering the question, "What is a buyer in this specific market willing to pay for that feature, right now?" An extra bathroom in a high-end suburban neighborhood won't have the same value as one in a dense urban condo market. It's all local.

So, what are we usually adjusting for?

- Gross Living Area (GLA): This is almost always the biggest one. You'll need to figure out a credible price per square foot based on recent sales and apply that to the difference in size.

- Bedrooms and Bathrooms: A home with four bedrooms is fundamentally different from one with three. Same for a second full bath versus a powder room.

- Lot Size: This can be a huge value driver, especially in areas where land is scarce or large yards are in high demand.

- Garage Capacity: The market clearly sees a difference between a one-car and a two-car garage. You need to quantify it.

- Condition and Upgrades: This is more subjective but critically important. Did the comp have a brand-new chef's kitchen, while your subject property has original 1980s cabinets? That’s a major adjustment.

The process is straightforward: identify the difference, assign a credible dollar value to it, and apply it to the comp's sale price.

The Golden Rule of Adjustments: If the comp is superior to your property (e.g., it has a pool and yours doesn't), you subtract the value of that feature from the comp's price. If the comp is inferior (e.g., it has one less bedroom), you add the value to its price.

Before you can even think about adjustments, though, you need a solid set of comps. This infographic breaks down the workflow for finding and categorizing them properly.

As you can see, a thorough analysis looks at everything—what sold, what’s on the market now, and what failed to sell. This gives you the full picture of past performance, current competition, and where the market's pricing ceiling might be.

Bringing It All Together

Once you've made these line-item adjustments for every key difference, each of your comps will have a new "adjusted sale price." This isn't just a random number; it's a calculated estimate of what that home would have sold for if it were just like yours.

Let's look at a quick, simple example:

- Subject Property: 3 bed, 2 bath, 1,800 sq ft, 2-car garage.

- Comp 1: Sold for $450,000. It's very similar, but it has an extra half-bath, which we've determined is worth about $5,000 in this market.

- Adjustment: The comp is superior, so we subtract that value.

- Adjusted Price for Comp 1: $450,000 - $5,000 = $445,000

You do this for all three to five of your chosen comps. When you're done, you should see a tight cluster of adjusted prices. Maybe they come out to $445,000, $452,000, and $448,000. That narrow range is a powerful indicator that you're zeroing in on the true market value.

Calculating the Final Value Range

With your adjusted prices ready, it's time to land on a final number. I rarely just take a simple average. Instead, I use a weighted average.

The comps that needed the fewest adjustments get more weight in my final calculation. Why? Because a property that was already very similar to start with is a much more reliable benchmark than one I had to adjust heavily.

This final figure is the core of your CMA. It's the number you can confidently stand behind because you have a logical, documented process to show how you got there. This is what you'll use to build your pricing recommendation. For a deeper dive into this final step, check out our complete guide on how to price a home for sale for more strategies.

This meticulous adjustment process is what turns a simple list of nearby sales into a genuine, professional market analysis. It's the work that builds trust with your clients and leads to a listing that’s priced right from day one.

Bringing It All Together: Assembling and Presenting Your CMA Report

All the number-crunching and meticulous research won't mean a thing if you can't present your findings in a way that makes sense to your client. A truly effective CMA report is more than just a dump of data; it's a story. Your job is to guide the client from a simple understanding of their own home to a logical, well-supported price.

Think of the final report as your closing argument. It needs to be professional, clean, and persuasive, turning raw data into a clear path forward for your client's big decision.

Structuring Your Report for Maximum Impact

A disorganized report is a recipe for confusion and doubt. To get your client on board, you need to structure your CMA with a clear, logical flow that builds your case one step at a time.

Every solid CMA report I've ever built includes these four key pieces:

- Subject Property Overview: Kick things off with the star of the show—the client's home. Include great photos, a compelling property description, and all the core stats you gathered (square footage, bed/bath count, lot size, etc.).

- Comparable Property Profiles: Next, introduce the supporting cast. Dedicate a clear section to each comp with photos, key details, and most importantly, the final sale price. I always include a map showing the comps in relation to the subject property; it’s a simple visual that really helps clients see the proximity.

- The Adjustment Worksheet: This is where the magic happens and where you prove your expertise. Lay out every adjustment in a simple table. This transparency is critical—it shows your client exactly how you accounted for the differences between their home and the others.

- Market Summary & Price Recommendation: Wrap it all up with a concise summary of the current market. Mention any active or pending sales that add context. Finally, present your suggested value as a tight price range, then land on a specific, recommended list price.

This structure allows the client to follow your logic, see the "why" behind your number, and ultimately trust your recommendation. To brush up on writing compelling narratives for your listings, check out these excellent property description samples.

Presenting Your Findings with Confidence

The way you deliver the CMA is just as important as the document itself. This is your chance to shine and solidify your role as the go-to market expert. Never just email the report and hope they "get it." Always schedule a time to walk through it together, whether it’s at their kitchen table or over a video call.

When you present, explain your process in simple terms. Show them the comps and explain why you picked them—and just as importantly, why you left others out. Walk them through the biggest adjustments you made. It's an educational process that demystifies pricing and builds incredible trust.

Your presentation should be a conversation, not a lecture. Encourage questions and be prepared to defend your conclusions with data. When a client understands the logic, they feel confident in the strategy.

The work you put in here has a real, measurable impact. Homes priced correctly from the get-go simply perform better. For instance, a 2023 National Association of Realtors (NAR) study found that homes listed within 5% of their CMA value sold a whopping 23% faster than homes priced outside that window. The average time on the market was just 32 days versus 41 days for the others.

For more general advice on making your delivery as sharp as your data, take a look at these helpful tips for creating a good presentation.

By assembling a clear, logical report and presenting it with confidence, you do more than just suggest a price. You empower your clients with knowledge, earn their trust, and set them up for a successful sale.

Answering the Tough Questions About CMAs

Even when you have a solid process down, certain questions always seem to surface. Getting comfortable with the answers not only builds your own confidence but also helps you articulate the finer points to your clients. Let's walk through a few of the most common ones I hear in the field.

How Is a CMA Different from an Online Home Value Estimator?

This is the big one. Almost every client will ask about the Zestimate they saw on Zillow or another online estimate. I tell them to think of those numbers as a conversation starter, not the final word.

Those online tools are what we call AVMs, or automated valuation models. They run on algorithms and public data, which is great for a quick, ballpark figure. But an algorithm has never walked through a house. It can't see the stunning new quartz countertops, smell the musty shag carpet in the basement, or hear the constant hum from the highway just beyond the backyard.

That’s where a real CMA comes in. We’re doing a manual, thoughtful deep dive. We hand-pick the absolute best comps and make nuanced, subjective adjustments for all those little things an algorithm will always miss. The result is a valuation that’s not just more accurate, but one we can actually stand behind and defend.

How Many Comps Should I Use in My Analysis?

There's no single magic number, but a good rule of thumb is to anchor your analysis with three to five really strong, recently sold properties. This gives you a solid foundation without muddying the waters with homes that aren't truly comparable.

Remember, quality will always beat quantity here. I’d much rather have three perfect comps that mirror the subject property in location, size, and condition than ten mediocre ones that force me to make huge, speculative adjustments. Once you have those three to five solid "solds," you can bring in a couple of active or expired listings to paint a fuller picture of the current competition and what the market won't bear.

What Should I Do If There Are No Recent Comps in the Area?

This happens more often than you’d think, especially with one-of-a-kind properties or homes in rural areas. When the ideal comps just aren't there, the trick is to broaden your search criteria—but do it systematically.

Don't just randomly jump to the next town over. Follow a logical progression:

- Go Back in Time: First, try pushing your search from the usual 3-6 months back to 9 or even 12 months. An older sale is almost always better than no sale.

- Expand the Map: If that doesn’t work, slowly widen your geographic radius. Look for an adjacent neighborhood that feels similar, with comparable schools and amenities.

- Make Bigger Adjustments: You might have to rely on less-similar properties. This means you’ll be making larger, more significant adjustments for things like square footage or lot size.

When you have to stretch your search this far, documenting your process is crucial. In your CMA report, make a note explaining why you chose those comps and the rationale for expanding your search. This transparency shows your client you’ve done the heavy lifting and builds a ton of credibility.

How Often Should a CMA Be Updated?

A CMA is a snapshot of the market at a specific moment, and its relevance can fade surprisingly fast, particularly when the market is hot. How long it’s “good for” really depends on the context.

For a homeowner who’s just curious about their equity, pulling a fresh CMA once a year is probably fine. But for an actively listed property, you should be refreshing the analysis every 30 days at a minimum. A new comp hitting the market, a sudden shift in local inventory, or a jump in mortgage rates can all move the needle on a property’s value. Keeping your analysis current ensures your pricing strategy stays sharp.

Putting together a fast, accurate, and professional CMA is the bedrock of any good pricing strategy. With Saleswise, you can generate a detailed, client-ready comparative market analysis in about 30 seconds. Imagine skipping the hours of digging for comps and wrestling with manual adjustments. Try Saleswise with a $1 seven-day trial and see for yourself how much it can sharpen your market intelligence.