How to Calculate Property Value Like a Pro

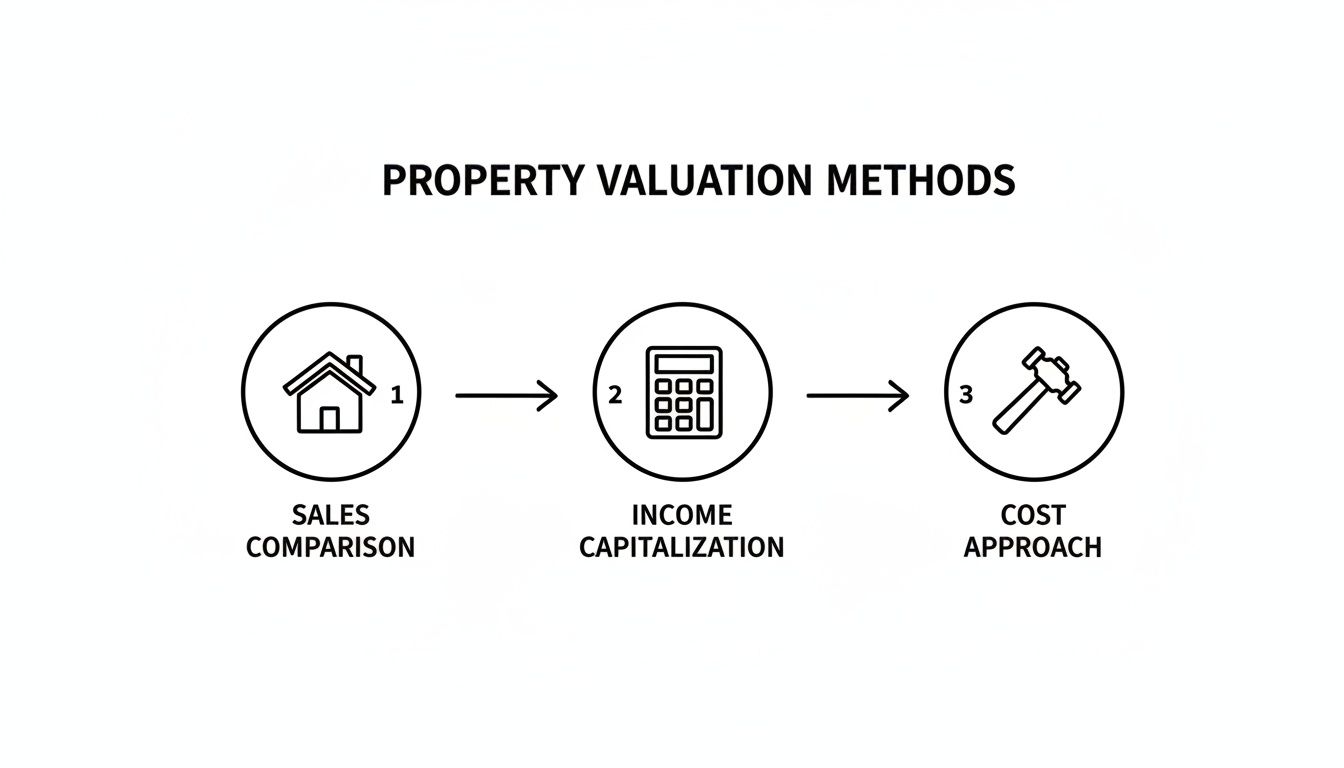

When you're ready to calculate a property's value, it all boils down to three tried-and-true methods: the Sales Comparison Approach, the Income Approach, and the Cost Approach. The trick isn't just knowing what they are, but knowing when to use each one. Choosing the right tool for the job is the first step toward an accurate valuation.

The Three Core Methods For Valuing Property

Moving past what a Zestimate says means thinking like a professional appraiser. These methods aren't just academic—they're the foundation for building a defensible, market-based price that builds client trust and gets a home priced correctly from the start.

If you pick the wrong approach, your numbers can be way off. Think of them as different lenses for looking at the same property; each one gives you a unique and necessary perspective.

When To Use Each Valuation Method

Context is everything in real estate, and valuation is no exception. Here’s a quick look at where each method really works best:

Sales Comparison Approach: This is your bread and butter for almost all residential real estate. For single-family homes, townhouses, and condos, you'll almost always find enough recent, similar sales to build a powerful case for a specific value. It's the most direct reflection of what the current market is willing to pay.

Income Approach: Got a property that makes money? This is your method. It's built for anything from a duplex to a large apartment building or a commercial storefront. The property's value is directly tied to the revenue it can generate, and this approach proves it.

Cost Approach: This one's for the oddballs and the brand-new builds. When you're dealing with a truly unique custom home, new construction, or a special-use building like a church or a school, you won't find good comps. So, you calculate what it would cost to build the same structure from the ground up today.

By getting comfortable with all three, you’re ready for anything a client throws at you, from a straightforward suburban ranch to a one-of-a-kind architectural gem. It’s all about applying the right logic to the right situation.

Ultimately, knowing how to calculate property value isn't about one magic formula. It's a strategic process. For a deeper dive, you can learn more about these real estate property valuation methods in our detailed guide. This knowledge is what separates a good agent from a great one, allowing you to create analyses that win listings and close deals.

Mastering the Sales Comparison Approach for Homes

When you're trying to pin a value on a residential home, the Sales Comparison Approach is your most reliable tool. It’s the method that gets right to the heart of what real buyers are willing to pay in today's market, making it the bedrock of any solid Comparative Market Analysis (CMA).

The idea is straightforward: a home's worth is directly tied to what similar, nearby houses have recently sold for. We call these "comps," and they're the key to everything. The real art isn't just pulling a list of sold properties; it's in the careful selection and adjustment of those comps. This is where your expertise as an agent moves from guesswork to a data-driven valuation that clients can actually trust.

This diagram shows how the three main valuation methods fit together. For the homes we deal with every day, the sales comparison path is the one we'll walk.

As you can see, our focus is distinct from the income or cost methods, which are better suited for different kinds of real estate, like commercial buildings or new construction.

Selecting the Best Comps

Let's be clear: your entire analysis hinges on the quality of your comps. Choose poorly, and you risk an inaccurate valuation that could cost your client dearly or leave a property sitting on the market for months.

Here’s what I always focus on when I'm hunting for the best comparable properties:

- Proximity is King: Stick to the same subdivision or immediate neighborhood. The moment you cross a major road, a school district line, or even a different zip code, values can shift dramatically.

- Recent Sales Only: The market moves fast. You should be looking at homes sold in the last three to six months, max. Anything older, especially in a dynamic market, is practically ancient history.

- Like for Like: This one sounds obvious, but it's crucial. Compare a two-story colonial to other two-story colonials. Keep square footage within a 10-15% range. The same goes for bedroom/bathroom counts and lot size.

- Condition Matters: You have to be honest about the property's state. If your client's home has a kitchen straight out of the 90s, you can't use a comp with a brand-new gourmet remodel without making some serious adjustments.

The Art of Adjusting Comparables

Once you’ve got your three to five best comps lined up, the real analysis begins. Since no two homes are ever truly identical, you need to make adjustments to level the playing field.

The rule of thumb is simple:

- If the comp is superior to your subject property (e.g., it has a pool and yours doesn't), you subtract the value of that feature from the comp's sale price.

- If the comp is inferior (e.g., your property has a two-car garage and the comp only has one), you add the value of that feature to the comp's sale price.

Think of it this way: you’re financially tweaking each comp to make it look as much like your client’s house as possible.

To make this clearer, here’s a quick guide on how to think about some common adjustments.

Comparable Property Adjustment Guide

This table shows some real-world examples of how to apply these adjustments to get a more accurate valuation.

| Feature Difference | Adjustment Direction | Example Calculation | Agent Tip |

|---|---|---|---|

| Finished Basement | Comp has one, yours doesn't | Subtract $15,000 from comp's sale price. | The market value of a finished basement varies wildly. Check recent sales with and without one to find a local baseline. |

| Extra Bathroom | Your property has an extra half-bath | Add $5,000 - $8,000 to comp's sale price. | A full bath adds significantly more value than a half-bath. Be specific in your calculations. |

| New Roof | Your property has a new roof | Add $10,000 to comp's sale price. | Major capital improvements like a new roof or HVAC system are high-value additions that buyers notice. |

| Outdated Kitchen | Comp has a renovated kitchen | Subtract $20,000 - $30,000 from comp's sale price. | Be realistic. "Renovated" can mean anything from new paint to a full gut job. Adjust based on the actual scope of work. |

Making these adjustments is how you build a powerful, logical case for your recommended price. For a more detailed walkthrough, you can check out our complete guide on how to do a comparative market analysis.

A great CMA tells a story. Every adjustment you make is a plot point that explains how you arrived at the final number. It’s about showing your work and building undeniable confidence with your client.

Common Mistakes to Avoid

Even experienced agents can slip up. One of the most frequent errors is using stale data in a market that's heating up or cooling down. For example, in a market like Los Angeles where median sale prices once shot up 8.5% in a year, a comp that's six months old is already misleading. This method is trusted in over 90% of residential appraisals precisely because it demands current data.

Another classic pitfall is trusting listing photos to judge a property’s condition. That "newly renovated" kitchen might just be freshly painted cabinets and cheap hardware. If you can't rely on your own knowledge of the property, dig into the agent-only remarks in the MLS for the real story. Nailing these details is what separates a guess from a professional valuation.

Using the Income Approach for Investment Properties

When you’re working with an investor, the conversation is completely different. Forget curb appeal and school districts for a moment. The only things that matter are cash flow, operating costs, and the potential return. This is exactly where the Income Approach comes in.

It's the go-to valuation method for any property that's meant to make money—think duplexes, small apartment buildings, or commercial rentals.

The entire approach boils down to a simple but powerful formula: Value = Net Operating Income (NOI) / Capitalization Rate. It’s a direct line connecting a property's ability to generate cash to its current market value, giving investors the hard numbers they need.

Calculating Net Operating Income

First things first, you have to figure out the Net Operating Income (NOI). This number is the property's annual income after you've paid all the necessary operating expenses but before you factor in things like a mortgage payment or income taxes.

To get the NOI, you start with the Gross Potential Income (GPI), which is what you'd collect if every single unit was rented out for the entire year. From there, you subtract two critical things:

- Vacancy and Credit Losses: Let's be real—no property is ever 100% occupied. A realistic vacancy rate, often somewhere between 5-10% of the GPI, accounts for the time between tenants and any unpaid rent.

- Operating Expenses: These are simply the costs of keeping the lights on and the property running smoothly.

Your typical operating expenses will include:

- Property Taxes

- Insurance Premiums

- Maintenance and Repairs

- Utilities (if the owner pays them)

- Property Management Fees

It's crucial to leave out costs like mortgage principal and interest, major capital expenditures (like a brand new roof), and depreciation. NOI is purely about how profitable the building itself is, regardless of the owner's financing situation.

For any investment property, maximizing potential income is key. For a deeper dive, understanding revenue management in rental properties shows how smart rental rate strategies can directly boost your NOI and, in turn, the property's value.

Finding the Right Capitalization Rate

The other half of the equation is the Capitalization Rate, or cap rate. This is the expected rate of return on the property based on the income it generates. You can think of it as a snapshot of the current market—what are other investors willing to pay for similar properties in this area?

A lower cap rate usually means a higher property value and less risk, while a higher cap rate suggests a lower value and more risk. For example, a sought-after property in a stable neighborhood might trade at a 4-5% cap rate, but a riskier property in a transitioning area could have a cap rate of 8% or even higher.

To find the right cap rate, you need to look at recent sales of comparable income-producing properties nearby. For each one, you'll calculate its cap rate with the same formula: Cap Rate = NOI / Sale Price. By averaging the cap rates from a few solid comps, you can land on a defendable rate for the property you're evaluating.

Putting It All Together: A Practical Example

Let’s run the numbers on a hypothetical four-plex where each unit rents for $1,500 a month.

- Gross Potential Income (GPI): 4 units x $1,500/month x 12 months = $72,000

- Vacancy Loss (at 5%): $72,000 x 0.05 = $3,600

- Effective Gross Income (EGI): $72,000 - $3,600 = $68,400

Now for the annual operating expenses:

- Property Taxes: $7,000

- Insurance: $2,500

- Repairs & Maintenance: $4,000

- Property Management (8% of EGI): $5,472

- Total Operating Expenses: $18,972

Next, we get our NOI: $68,400 (EGI) - $18,972 (Expenses) = $49,428.

After pulling comps, we’ve found that similar buildings in the neighborhood are selling at an average 6% cap rate. Now we have everything we need.

Finally, we calculate the value: $49,428 (NOI) / 0.06 (Cap Rate) = $823,800.

This is the kind of solid, data-backed valuation your investor client is looking for. It’s based entirely on the property’s financial performance, giving them a clear picture of what it's truly worth.

Applying the Cost Approach for Unique Properties

While it’s not the method you’ll pull out for every suburban home, the Cost Approach is a critical tool in your valuation arsenal. It’s built on a beautifully simple premise: a property's value is what it would cost to build an identical one from scratch today.

You’ll find yourself turning to this approach when reliable comps are nonexistent. Think about valuing a brand-new custom build, a unique architectural home, or even special-use buildings like a school or a church. In these cases, the Sales Comparison Approach just doesn't work because there's nothing truly comparable. That's when the Cost Approach becomes your best friend, giving you a logical way to build a valuation from the ground up.

Knowing how to use it means you're prepared for any curveball a client throws at you. It rounds out your expertise and provides a solid, defensible number when comps are thin on the ground.

Calculating Value with the Cost Approach

The process itself is surprisingly straightforward. It follows a clear formula that cuts through market noise and focuses entirely on the hard numbers. Think of it as constructing the property on paper.

The core formula looks like this:

Property Value = Land Value + Replacement Cost – Depreciation

Let's break down each piece.

Find the Land Value: The first step is to figure out what the land itself is worth, as if it were an empty lot. You’ll lean on the sales comparison method for this part, analyzing recent sales of similar vacant parcels in the neighborhood.

Estimate the Replacement Cost: Next, you need to calculate the cost to build a comparable structure today, using current labor rates and material prices. This information is readily available in construction cost handbooks or specialized software.

Subtract All Depreciation: This is where the real expertise comes in. You have to account for any loss in value, which goes beyond simple wear and tear. Depreciation includes functional obsolescence (like a clunky, outdated floor plan) and external obsolescence (like a new highway built next door that adds noise).

The appraisal of real estate is, as one court noted, “at best an imprecise art” and an “inexact science.” The Cost Approach provides a scientific framework, but accurately judging depreciation requires an artistic touch and deep market knowledge.

When you get comfortable with this method, you'll never feel caught off guard. You can confidently price anything that comes your way, from a standard tract home to a one-of-a-kind estate.

How AI Tools Can Seriously Speed Up Your Valuations

Knowing how to build a CMA from scratch is a foundational skill for any agent. But let's be honest, it's a grind. Digging through the MLS, hand-picking comps, and then making all those tiny adjustments for a finished basement or an extra bathroom takes hours.

Every minute you're buried in spreadsheets is a minute you're not in front of clients, and in a fast-moving market, that's a huge disadvantage. This is where the right technology can be a game-changer. Modern AI platforms don't replace your expertise; they amplify it by taking the most tedious, time-sucking parts of the valuation process off your plate.

From Hours of Work to a 30-Second Report

What if you could shrink the entire CMA process—from finding comps to having a polished, client-ready report in hand—down to less than a minute? That’s exactly what AI-powered tools are designed to do.

A platform like Saleswise plugs directly into live market data, instantly pulling the most relevant sold and active comparables for your subject property.

Instead of you manually filtering through dozens of listings, the algorithm handles the heavy lifting. It crunches the numbers on proximity, sale dates, square footage, and other key features to give you a pre-vetted list of the best comps out there. This not only saves you a ton of time but also minimizes the risk of overlooking a key property or making a simple mistake.

The result? You get a detailed, professional report generated in about 30 seconds. This frees you up to focus on what really matters: advising your clients and closing deals.

Gaining an Edge with Smarter Data and Better Presentation

Speed is great, but accuracy is everything. AI-driven valuations bring a level of precision that’s tough to match manually. By analyzing thousands of data points at once, these systems can spot patterns and reduce the unintentional bias that sometimes creeps into our own comp selections.

Beyond the numbers, the output is designed to impress. You’re not just handing over a spreadsheet; you’re presenting a visually compelling, easy-to-understand report that clearly walks your client through the valuation. This builds immediate trust and positions you as a data-savvy expert.

The real magic of AI here is how it turns raw market data into a persuasive story. When you can present a beautiful, data-backed CMA just minutes after a listing appointment, you leave a lasting impression and create a serious competitive advantage.

The Bigger Picture: Your AI Toolkit

Valuations are just the beginning. The world of AI in real estate is growing fast, and there are many ways to put it to work. For a deeper dive, you can check out some of the best AI tools for real estate professionals.

Beyond CMAs, these tools can help you win and market listings more effectively. Here are a few things they can do:

- AI-Powered Content: Instantly write captivating listing descriptions, marketing emails, and social media captions that grab attention.

- Virtual Staging: Help buyers see a home's full potential with realistic virtual staging or room remodels.

- Deeper Market Insights: Access neighborhood-level trends and analytics to sharpen your pricing strategies.

By weaving these tools into your workflow, you can become much more efficient. To learn more about how to get started, take a look at our guide to AI tools for real estate agents. In today's market, using this technology isn't just a nice-to-have—it's becoming essential for staying ahead of the curve.

Your Top Property Valuation Questions, Answered

Once you have the fundamentals down, the real learning happens in the field. Every property is unique, and homeowners always have questions. Being ready with clear, confident answers is what separates a good agent from a great one.

Here are a few of the most common curveballs you'll get from clients and how to handle them.

Tax Assessment vs. Market Value: What’s the Difference?

This one comes up all the time, and it’s a major point of confusion for sellers. They see their tax bill and think that’s what their home is worth.

The tax-assessed value is just a number the local municipality uses to figure out property taxes. They typically use mass appraisal models, which are basically algorithms that estimate value for entire neighborhoods at once based on broad data like square footage and year built.

Market value is completely different. It’s the price a ready and willing buyer would actually pay for the home right now. A tax assessment can’t see the brand-new kitchen, the beautiful landscaping, or factor in the current low inventory driving prices up. That's why it's often way off the mark—and why you should never, ever use it in a CMA.

What Exactly Is Home Equity?

Think of home equity as the owner’s actual stake in the property. It’s the slice of the home's value they own outright, separate from what the bank is owed. The math is simple: Current Market Value - Remaining Mortgage Balance = Home Equity.

So, if you determine a home’s market value is $500,000 and the owner has a $300,000 mortgage balance, their equity is $200,000. This number is hugely important for sellers because it’s the foundation of their net proceeds—the cash they'll walk away with after the sale.

Your market valuation is the starting point for everything. Without an accurate, well-researched value, any conversation about a seller's equity is just a shot in the dark.

How Much Are My Renovations Really Worth?

Every seller who has put money into their home wants to know this. The truth is, not all upgrades are created equal, and you rarely get a dollar-for-dollar return.

A major kitchen or primary bath remodel can certainly move the needle, but a new roof is mostly about maintaining value, not adding to it. It’s an expectation, not a bonus feature that makes a buyer want to pay more.

The best advice you can give is to focus on what today’s buyers in your local market actually want. Often, the highest ROI comes from smaller, cosmetic touches like a fresh coat of neutral paint or updated light fixtures. These low-cost improvements make a home feel current and help it stand out against the competition.

Ready to build CMAs that win listings? Saleswise uses AI to create stunning, client-friendly property valuations in about 30 seconds. It pulls live data and presents it beautifully, so you look like the expert you are. Start your $1 trial of Saleswise today and see the difference it makes.